Potential Topics at the Forefront of Coronavirus Coverage Disputes

Insurers will likely see an influx of claims due to the COVID-19 pandemic. Advance preparation for these claims and the coverage issues they potentially involve will help insurers navigate through the deluge of claims and suits likely to follow. This article discusses five main topics at the forefront of coverage litigation concerning novel coronavirus claims.

Business Interruption Coverage:

First-party insurers will likely be inundated with claims from businesses seeking recovery under business interruption provisions in their policies.

There are many forms of business interruption coverage and both insurers and their counsel should be mindful of their differences. However, the general purpose of business interruption coverage is to reimburse the policyholder for lost profits and fixed costs associated with operation of a business during the period of restoration from the interruption.

It is a common misconception that property insurance provides standalone coverage for business interruption losses. Property insurance policies commonly provide coverage for business interruption losses solely to the extent that the interruption results from covered property damage. In other words, a policyholder must first demonstrate the existence of covered property damage and can only then seek insurance recovery for business interruption losses flowing from that property damage.

Thus, the question turns on whether the coronavirus causes physical damage to property. Most courts find that in order to trigger business interruption coverage, there must be “direct physical loss of or damage to the property at the premises described in the Declarations.” On its face, this requirement does not appear to be satisfied by a mere claim of a general decline in economic activity due to a pandemic.

Insurers and their counsel should prepare for policyholder arguments that contend “direct physical loss of or damage to the property” has occurred by the mere presence of the coronavirus at the premises. It is not unexpected that policyholders will argue that to the extent the coronavirus has infiltrated a premise, the loss of functionality of the property is akin to physical loss or damage. All parties should be aware of the highly scientific and technical aspect of proving such a theory when pursuing and defending against such claims.

Civil Authority Clauses:

In conjunction with the business interruption coverage, policyholders may also seek coverage for losses under a “civil authority clause.” A civil authority clause, also known as a “public authority clause,” is a provision that outlines how the loss of business income coverage applies when a government entity denies access to the insured property.

In the recent weeks, we have seen state and local authorities order the closing of bars and restaurants, or limiting services offered by these businesses, in order to thwart the spread of the coronavirus. Thus, insurers are likely to see business interruption claims based upon the “civil authority clause.”

Similar to business interruption coverage, however, the civil authority clause requires that the government restriction stem from a “direct physical loss” or damage to a nearby property for the coverage to apply. A policyholder would have to show the coronavirus actually caused physical damage to a nearby property. Policyholders may face a tough task in fulfilling the direct physical loss requirement, especially where the science around the spread of the coronavirus is unsettled and still evolving.

Event Cancellation Coverage:

In the past week, high-profile event cancellations have become a near-daily occurrence. Insurers will likely receive inquiries from event organizers seeking guidance on coverage under event cancellation policies, which generally cover at least some of the policyholder’s lost revenue and out-of-pocket expenses.

These specialized policies almost always contain a list of covered causes, some of which may include “communicable diseases,” or even more specifically, pandemics. However, Insurers should review its policy’s provisions to see whether the policy applies if an organizer cancels merely due to the fear of coronavirus in the community.

The policies are designed to respond in cases where there is a legal or physical impossibility of holding the event. They do not kick-in when a policyholder makes the voluntary decision not to go forward with an event. Therefore, if an organizer cancels an event due to an official ban on large public gatherings, they are more likely to be eligible for coverage. If they decide to do so without such a directive, coverage may not be afforded.

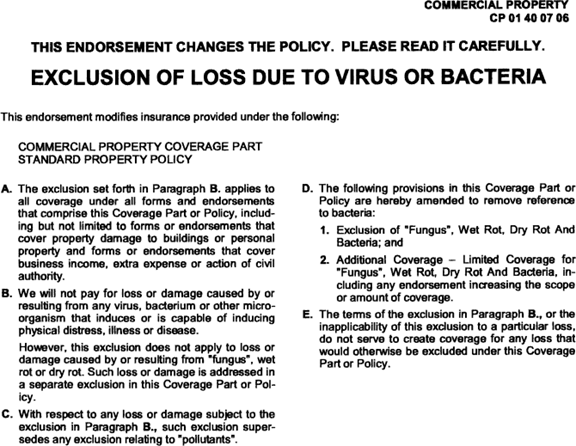

Application of “Exclusion—Loss Due To Virus Or Bacteria”

Many business interruption policies contain an exclusion for “Loss Due To Virus Or Bacteria,” ISO Form CP 01 40 07 06.

The ISO’s July 6, 2006 circular, prepared as part of its filing of the exclusion with state regulators, makes specific reference to viral and bacterial contaminants such as rotavirus, SARS, influenza, legionella and anthrax.

The exclusion goes on to specifically state that it applies to, among other things, business income and extra expense or action of civil authority. The exclusion is meant to apply even if the presence of coronavirus satisfies the “direct physical loss or damage to” requirement. Insurers should be mindful whether this exclusion is a part of its policies when analyzing claims due to the coronavirus pandemic.

General Liability:

First-party property insurers are not the only potential carriers that will likely see claims. General liability insurance carriers will likely see claims alleging failing to protect customers from the coronavirus, and in extreme cases, claims under “personal and advertising injury” liability coverage.

As companies begin to take action to minimize the harm of the virus, a failure to do so may give rise to liability. We have seen businesses close to avoid the spread of the virus. Any similar business that chooses to remain open or has no plan in place to protect its employees could later be viewed as negligent.

Claims of negligence resulting in “bodily injury” typically fall under Coverage A of standard general liability policies. However, one of the prerequisites for coverage under that prong is that there be an accidental “occurrence.” Thus, there will likely be a debate around whether there was an accident in these types of cases and whether alleged “bodily injury” is caused by an intended deliberate act.

Additionally, policyholders could potentially see claims under Coverage B for personal injury offenses such as false detention and imprisonment if claimants were improperly detained and quarantined.

Even if an insured succeeds in triggering coverage under one or both insuring agreements of a general liability policy, insurers should consider exclusions relating to “property damage” or “bodily injury” stemming from exposure to a “pollutant” or “contaminant” as some jurisdictions could potentially interpret these terms broadly enough to encompass the coronavirus.

* * *

As concerns about the novel coronavirus continue to grow, those practicing in insurance coverage will no doubt have to wrestle with differing opinions whether the damages and losses arising from the pandemic are covered under insurance policies. Determining whether coverage exist will require careful analysis of the specific policy language as applied to the unique facts of each claim. An understanding of what to expect and look for will help insurers navigate through these expected and inevitable claims.

Please feel free to contact me with any questions.